Corporate governance report

PRINCIPLE ONE – GOVERNANCE STRUCTURE

OUR PHILOSOPHY

The Board of Directors (Board) deems that endorsing quality norms and beliefs of corporate governance in the Bank provide a solid bedrock for sustainability, a long haul value creation for all of its stakeholders and promote a culture of debate and openness. The Board is entrusted with the powers through its leadership in the hierarchy eulogising elevated standards of corporate governance to direct and supervise the conduct of the business and the affairs of the Bank ethically and effectively.

OUR GOVERNANCE FRAMEWORK AND ACCOUNTABILITIES

ABL, a public company incorporated on 12 January 2007, holds a Banking Licence which was issued on 29 August 2007. Its core banking and transactional capabilities are in Mauritius along with a representative office in South Africa. It is a Public Interest Entity (“PIE”) as per the Financial Reporting Act 2004 and is in line with the requirements of the relevant rules, regulations and legislations.

The Bank operates under the aegis of a unitary board, collectively geared in guiding and directing the organisation to take the necessary steps to adhere, to the best of the Board’s knowledge, to all legal and regulatory requirements, such as:

- The eight principles issued by the National Committee on Corporate Governance in its “National Code of Corporate Governance 2016”;

- The Banking Act 2004 (amended March 2019) issued by the Bank of Mauritius;

- The “Guidelines on Corporate Governance 2001” (revised October 2017) issued by the Bank of Mauritius (BOM); and

- The provisions of the Mauritius Companies Act 2001.

Throughout the year ended 30 June 2019, the Bank has complied with all the principles set out in the Code and explained how these principles have been applied to the exception of the required board appraisal exercise (Principle 4) that could not be undertaken due to recent changes in the Bank’s directorship.

Disclosures pertaining to the eight principles of the Code have been made in different sections of the Annual Report, as outlined below:

| Principles of the Code | Relevant sections of the Annual Report |

|---|---|

| Principle 1: Governance Structure | Corporate Governance Report |

| Principle 2: The Structure of the Board and its Committees | Corporate Governance Report |

| Principle 3: Director Appointment Procedures | Corporate Governance Report |

| Principle 4: Director Duties, Remuneration and Performance | Corporate Governance Report |

| Principle 5: Risk Governance and Internal Control | Corporate Governance Report and Risk Management Report |

| Principle 6: Reporting with Integrity | Corporate Governance Report, Sustainability Report and Finance Statements |

| Principle 7: Audit | Corporate Governance Report |

| Principle 8: Relations with Shareholders and Other Key Stakeholders | Corporate Governance Report |

ABL has in place a Conduct and Ethics Policy and in line with same, it is committed to employing great people and to promote a culture of mutual respect and ethical behaviour. Employees and Directors are expected to treat each other with consideration and respect and are not permitted to engage in conduct which is hostile or offensive to another person. The Bank promotes transparency and all staff and Directors are made aware and accountable of their responsibilities.

A copy of the Conduct and Ethics Policy is available on the Bank’s website.

OUR GOVERNANCE STRUCTURE

KEY GOVERNANCE POSITIONS

The Terms of Reference, which the Board approves and reviews as and when required, defines all key governance positions within the Bank and their corresponding accountabilities which are crucial drivers of strategic performance and optimised adherence to proper governance. A clear line of demarcation is drawn between the roles and responsibilities of the Chairperson and the Chief Executive Officer (CEO) to disrupt any unfettered powers; these are listed below:

SENIOR MANAGEMENT TEAM PROFILE

PRINCIPLE TWO – THE STRUCTURE OF THE BOARD AND ITS COMMITTEES

The Board is responsible for the overall stewardship of the Bank and thus plays a key role in ensuring that the appropriate level of corporate governance is maintained.

The powers of Directors are set out in the Bank’s Constitution and in the Terms of Reference for the Board first adopted in August 2007 and revised in June 2013. The Board is aware of its responsibilities to ensure that the Bank adheres to all relevant legislations such as the Banking Act 2004, the Financial Reporting Act 2004, the Financial Services Act 2007 and the Mauritius Companies Act 2001. The Board reassesses its Terms of Reference as and when required.

The Board also follows the principle of good corporate governance as recommended in the National Code of Corporate Governance 2016 and the BOM Guidelines on Corporate Governance 2001 (revised October 2017). It reviews and approves on a regular basis the Bank’s Code of Ethics to ensure that they are in line with the Bank’s objectives. It also regularly monitors and evaluates the Bank’s compliance with its Code of Ethics.

PRINCIPLE THREE – DIRECTORS’ APPOINTMENT PROCEDURES

BOARD MEMBER APPOINTMENT AND RE-APPOINTMENT

The Board has mandated the Corporate Governance Committee to select and review candidacies of the proposed Directors guided by legal and regulatory requirements. During the year under review, the Board has approved and adopted a policy, procedure and guidance for talent management, it is principally based on a number of objective criteria, for instance:

- Skills, knowledge and experience

- Independence of mind

- Needs of the Board at this period

- Board diversity

Once the selection process has been completed, it makes its recommendation to the Board for approval.

For the purpose of filling a casual vacancy, the Board may approve the proposal of the Corporate Governance Committee. As such, the proposed Director shall stay in office until the next following annual meeting whereby he/she can be appointed by the shareholders.

The board members’ selection and nomination process can be classified into the main steps illustrated below:

Identification

Identification and evaluation of the Board's needs

Profile

Profil of the ideal candidate.

Search

Search of potential and selection of candidate.

Nomination

Nomination of the selected candidate.

Appointment

Appointment of the candidate.

The newly appointed Director shall receive a Letter of Appointment whereby the following details are provided:

- Terms of Appointment

- Time Commitment

- Roles and Duties

- Outside Interests

- Confidentiality

- Price Sensitive Information and Dealing in the Bank’s Shares

- Induction

- Insurance

INDUCTION AND PROFESSIONAL DEVELOPMENT

Following appointment on the Board, the Directors receive an extensive and formal tailored induction training to familiarize themselves with the activities of the Bank. In addition to receiving an information pack, the Directors also get accustomed with the Terms of Reference of the Board and their statutory duties and obligations.

Directors also receive quarterly ongoing updates on regulatory changes, which includes briefings to Audit Committee members.

The Chairman ensures that the development needs of the Directors are identified and consequently appropriate training is provided to continuously update their skills and knowledge.

In line with continuous professional development, the Directors attended a workshop on IFRS 9 and its implications for the Bank during the year under review.

SUCCESSION PLANNING

In accordance with its Terms of Reference, the Board is responsible for the succession planning of the Board, the Chief Executive Officer and Senior Management of the Bank.

The Board has mandated the Corporate Governance Committee to put in place the succession plans, especially that of the Chairperson and of the CEO. Same has been formalised in the Terms of Reference of the Corporate Governance Committee.

The Corporate Governance Committee shall be responsible for the identification and selection of potential candidates.

PRINCIPLE FOUR – DIRECTORS’ DUTIES, REMUNERATION AND PERFORMANCE

BOARD APPRAISAL

The Board regularly undergoes a performance appraisal exercise, in accordance with the National Code on Corporate Governance for Mauritius and BOM Guidelines on Corporate Governance. The Directors are requested to evaluate the Board on the following main criteria:

- The Board’s size, composition and structure

- The Board’s roles, duties and responsibilities

- The effectiveness of the Board and its Committees

- The role and function of the Chairperson

The regular board appraisal exercise is performed internally through the Company Secretary, under the leadership of the Chairperson. It is generally done via questionnaires and the results are presented to the Corporate Governance Committee and ultimately, to the Board once they are available. The remarks and recommendations received are shared with the Board to enable the Directors to take appropriate steps where necessary and possible.

No Board appraisal exercise has been performed for the year under review due to recent changes in Board composition. The board regularly considers the need to conduct a board appraisal exercise.

The recommendation of the Code revolving around the use of an external consultant for Board appraisal exercises has been noted for forthcoming assessments.

DIRECTORS’ REMUNERATION AND BENEFITS

The Corporate Governance Committee acts as Remuneration Committee as and when required and as part of its duties it determines, agrees, develops and reviews the Bank's general policy on executive and senior management remuneration.

The Executive Director who is in full time employment with the Bank is entitled to a fixed salary as per his contract of employment and he does not receive any additional remuneration for attending the Board meetings and Committees.

The table below sets out the fee structure for Non-Executive Directors:

| Category of Member | MUR' 000 | Fee details |

|---|---|---|

| Board Member | 440 | Fixed fee per annum |

| Committee Member | 45 | Per attendance |

| Additional fee to Credit Committee Member | 540 | Yearly |

| Additional fee to Credit Committee Member | 15 | Per attendance |

| Additional fee to Chairman of Committee | 10 | Per attendance |

| Risk Committee Member being also a Credit Committee Member | 25 | Per attendance |

The Non-Executive Directors have not received any remuneration in the form of share options or bonuses associated with organisational performance during the year.

Total remuneration and benefits received and receivable, by the Directors from the Bank and its subsidiary for the year ended 30 June 2019 were as follows:

| YEAR ENDED 30 JUNE 2019 | YEAR ENDED 30 JUNE 2018 | YEAR ENDED 30 JUNE 2017 | ||||

|---|---|---|---|---|---|---|

| Executive Directors MUR ‘000 | Non-Executive Directors MUR ‘000 | Executive Directors MUR ‘000 | Non-Executive Directors MUR ‘000 | Executive Directors MUR ‘000 | Non-Executive Directors MUR ‘000 | |

| The Bank | ||||||

| AfrAsia Bank Limited | 17,975 | 8,089 | 17,546 | 7,346 | 18,311 | 6,152 |

| The Subsidiary | ||||||

| AfrAsia Capital Management Limited | 12,225 | - | 5,629 | - | 2,449 | - |

The detailed fees/remuneration paid to directors have been provided on page 53 of the Annual Report.

DIRECTORS’ SERVICE CONTRACTS WITH THE BANK AND ITS SUBSIDIARY

Sanjiv Bhasin, Executive Director of AfrAsia Bank Limited, has a service contract with the Bank for a period of five and a half years expiring on 30 June 2021 and thereafter renewable if agreed by both parties. The notice period for termination of the contract is six months.

Thierry Vallet, Director of AfrAsia Investments Limited, has a service contract with the Bank for an undetermined period, the notice period for termination of the contract is six months.

DIRECTORS’ SHARE INTEREST

The interests of the Directors in the securities of the Group and the Bank are maintained by the Company Secretary. As part of the appointment of a director, the latter needs to notify in way of writing to the Company Secretary their interests as well as their associates’ interests in the securities of the Group and the Bank.

The directors’ share interest as at 30 June 2019 were:

| YEAR ENDED 30 JUNE 2019 | YEAR ENDED 30 JUNE 2018 | YEAR ENDED 30 JUNE 2017 | ||||

|---|---|---|---|---|---|---|

| Ordinary Shares held directly and indirectlyNumber | Ordinary Shares held directly and indirectly % | Ordinary Shares held directly and indirectly Number | Ordinary Shares held directly and indirectly % | Ordinary Shares held directly and indirectly Number | Ordinary Shares held directly and indirectly % | |

| Jean Juppin De Fondaumiere (Chairperson) (Appointed on 8 January 2019) | - | - | - | - | - | - |

| Sanjiv Bhasin (Chief Executive Officer) | - | - | - | - | - | - |

| Jean Claude Béga (Resigned on 28 October 2018) | - | - | - | - | - | - |

| Martin Caron* (Appointed on 20 August 2018) | - | - | - | - | - | - |

| Henri Calvet (Resigned on 14 November 2018) | - | - | - | - | - | - |

| Dipak Chummun | - | - | - | - | - | - |

| Yves Jacquot | - | - | - | - | - | - |

| Philippe Jewtoukoff | - | - | - | - | - | - |

| Arnaud Lagesse* (Appointed on 5 November 2018) | - | - | - | - | - | - |

| Lim Sit Chen Lam Pak Ng* (Resigned on 14 November 2018) | - | - | - | - | - | - |

| Boon Huat Lee (Resigned on 15 February 2019) | - | - | - | - | - | - |

| Luc Paiement (Resigned on 20 September 2018) | - | - | - | - | - | - |

| Graeme Lance Robertson (Resigned on 16 August 2018) | 11,436,404 | 10.12 | 11,436,406 | 10.12 | 10,701,848 | 10.03 |

| Arvind Sethi | - | - | - | - | - | - |

| Mathew Welch* (Appointed 4 February 2019) | - | - | - | - | - | - |

| Francois Wertheimer (Appointed on 8 January 2019) | - | - | - | - | - | - |

*Those directors have opted to exclude notification of the interests of their associates in the securities of the Company and their interests and those of their associates in the securities of the associates of the Company.

The Directors do not hold any shares in the subsidiaries of the Bank whether directly or indirectly.

CONFLICTS OF INTEREST

Conflicts of interest is a situation whereby the interest of a member of the Board or Management or one of the significant shareholders and/or one of their associates is or may be competing with or impeding on the interests of the Bank and/or the Group.

Any conflict or potential conflict of interest must be declared to the Board and/or Company Secretary. The conflicts of interest of Directors are generally recorded in a register maintained by the Company Secretary. The Interest Register is available for consultation to shareholders upon written request to the Company Secretary.

It is noted that for any Board and Committee meetings, the agenda contains a standard item whereby the Directors present are requested to declare any interest that they have or may have with respect to any of the matters to be discussed. Any declaration made has been recorded in the minutes accordingly and the conflicted director has had to abstain from participating in the deliberations and from voting on the concerned matter.

The following principles are encouraged in relation to conflicts of interest:

- The personal interests of a Director or persons closely associated with the Director must not take precedence over the Bank and its shareholders, including the minority ones;

- Directors are required to avoid conflicts of interest and make full and timely disclosure of any conflicts of interest when exposed to same; and

- Directors appointed by shareholders are aware that their duties and responsibilities are to act in the best interest of the Bank and not for the shareholders who nominated them.

All information obtained by Directors in their capacity as Director to the Board of AfrAsia Bank Limited are treated as confidential matters and are not divulged to any other parties without the expressed authority of the Board.

INFORMATION TECHNOLOGY AND IT SECURITY

The Bank’s overall strategic direction is highly dependent upon its information technology management.

Businesses are today rapidly embracing new technologies and modern ways of working. Historically-separate domains no longer have the luxury of operating in a vacuum. Business competitiveness depends on business-technology alignment. As employees spend more time using their personal devices on premise, interacting on social networks, and sharing information via file-sharing services, the Bank has to look for ways to ensure security and data preservation while safeguarding privacy of the users. Newer generations understand this intuitively: the volume of information created and consumed on mobile devices is growing exponentially, which is also changing and shaping the way individuals use and share information.

With technology innovating and evolving much faster than the speed of change in organizational cultures, as they extend out to cloud and mobile devices, IT teams have to radically change how they operate. Most important is how they offer their services, including how they procure products and services, manage technology and data assets, together with their own role within the organization within a certain framework.

ABL’s technology leadership plays a key role to embrace this trend to deliver efficient and effective information technology that enables business development. Collective decision-making can result in executive buy-in to help drive more business value from technology investments, however, policy enforcement can fall short when the organization lacks tools to monitor and manage compliance of the Bank policies. Serious efforts are required from executives to enforce the required policies. In this respect, the Board has established a Board IT steering committee together with a set of governance policies which are implemented and regularly reviewed to manage, minimize the associated risks and align with the modern business world. The Board ensures that the Bank continuously seeks to foster a robust framework for the smooth running of its activities, together with adequate proficient resources and sophisticated infrastructure to manage the relevant risks and the business continuity of the Bank. As such continuous investments in people, technology and security is critical to upkeep with the competitive innovative landscape to remain relevant. The committee also strive to support modern ways of working.

Refer to the Risk Management Report set out on pages 84 to 113 of the Annual Report for information governance.

REMUNERATION PHILOSOPHY

The goal of AfrAsia Bank Limited is to be recognized as an employer of choice and as well as the most trusted financial partner in Mauritius and across Africa. Remuneration is a key vehicle towards achieving this objective, encouraging and enabling the Bank’s 400+ employees to deliver the best possible customer experience (CX) through enhanced employee experience (EX). Remuneration plays an essential role in attracting top-talent. On the path towards excellence, the best people are drawn from the broadest pool of applicants from both local and international markets. We offer a decent workplace in which the richness of their diversity and experience are both welcomed and valued by colleagues. The Bank promotes its culture through its values inculcating teamwork, a disruptive and innovative approach. AfrAsians are groomed to excel in their line of operations and expertise. Employees are encouraged to promote the highest ethical standards in their conduct, our internal policies promote integrity at all times and this is demonstrated through our overall business culture. At AfrAsia Bank Limited, we provide competitive remuneration and a variety of financial and non-financial benefits for our people. Our remuneration practice which adopts a total compensation approach, is based on strong governance, ensuring AfrAsia Bank complies with legislation and regulatory requirements while ensuring that as an organisation we remain agile and competitive on the market.

EMBEDDING CULTURE IN BUSINESS AND PEOPLE PROCESSES

Cultural change at AfrAsia Bank Limited is a multi-year journey, with strong senior management commitment and a clear tone from the top. Our organisational values were revamped in 2017 in order to be more in line with employees, a majority of which are millennials and digital natives. To make our values remain tangible our induction was also revamped whereby newcomers are exposed to experiential learning of our values. Moreover, refresher workshops are run on a regular basis for all employees where participants are given the opportunity to reflect and commit to living up the organisation’s values. These sessions help explain how the values relate to the bank’s vision, what the values and beliefs mean specifically in our everyday business transactions, client relationships and internal processes, and most of all how each employee can implement the values to bring about change in their department.

ATTRACT AND RETAIN TALENT

All employees are assessed using the balanced score card as a performance management online tool. Employees are not only assessed as to what they do through their objectives but also as to how they do what they do through the values assessment. In the aim to promote a high performance culture, the Bank recognises those who successfully execute their responsibilities - a high performance is reflected in comparatively higher rewards, as this ultimately helps the Bank meet its strategic targets. Rewards, benefits, policies and procedures are reviewed on a regular basis to ensure we attract the best talent as well as ensuring we remain aligned to the evolving market. The newly introduced Talent Management system is helping the Bank move another level in its management of talent. We provide career paths and more opportunities for internal moves and promotions. Worth highlighting that around 16% of employees were promoted of over the last 12 months and this figure has been increasing year in year. Investment in learning has been material and we believe in enhancing knowledge through soft and technical training and financial sponsorship to help towards growth in knowledge, skills and attitude. Quality of work life is key and work life integration is promoted along with flexible working arrangements.

PRINCIPLE FIVE – RISK GOVERNANCE AND INTERNAL CONTROL

- BOARD

- BOARD SUB-COMMITTEES AND EXECUTIVE MANAGEMENT

- RISK MANAGEMENT

- CORPORATE INTEGRITY AND WHISTLE BLOWING POLICY

-

BOARD

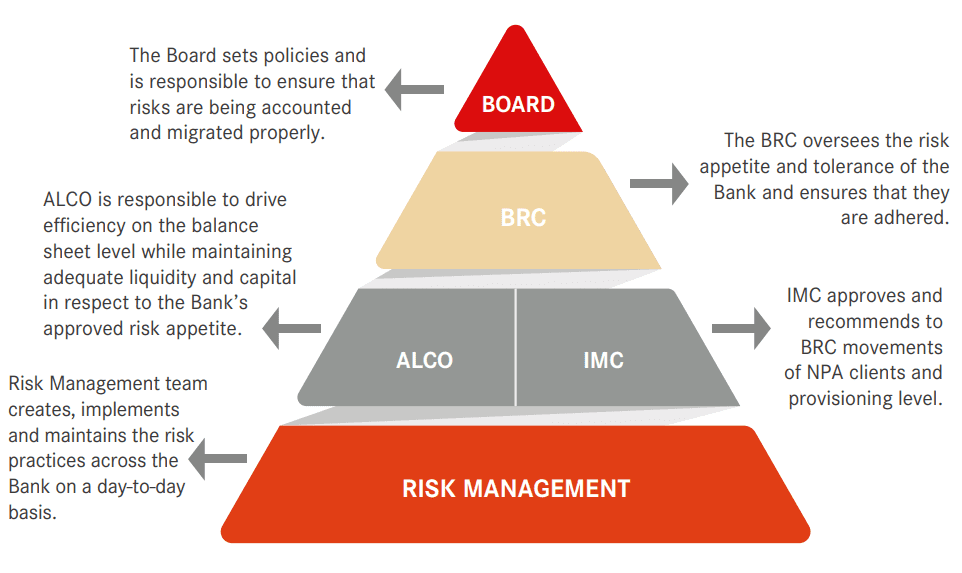

The Board leads the conduct of affairs and provides sound leadership to the executives of the Bank. It sets clearly defined policies and the Bank’s risk appetite, which are then conveyed to the executives via their delegated authorities to facilitate them to oversee the course of actions of the business. Additionally, the Board ensures that risks are being properly detected, managed and mitigated.

-

BOARD SUB-COMMITTEES AND EXECUTIVE MANAGEMENT

The Board Risk Committee (BRC) reviews the principal risks and has a global view on all risks that the Bank faces such as credit, market, liquidity, operational, legal, compliance and reputational risks. The BRC oversees that appropriate actions are being taken to mitigate or avoid these risks, all in compliance with Bank of Mauritius guidelines and policies approved by the Board. It also recommends the Board in respect to risk management issues, including limits setting and the Bank’s risk appetite framework. Moreover, the BRC is responsible to ensure that the Bank maintains a satisfactory liquidity and solvency ratio at all times.

The Assets & Liabilities Committee (ALCO) and the Impairment Committee (IMC) both report to the BRC on their operations. -

RISK MANAGEMENT

The risk management team, through its different divisions, monitors the day-to-day management of risk and promotes a robust risk culture across the Bank. It is responsible to create, implement and maintain the risk practices across the Bank as defined by the Bank’s risk appetite and to ensure that controls are in place for all risk categories.

The risk management team reports and provides recommendations on significant issues related to risk management, control and governance processes within the Bank to the BRC. It maintains its objectivity by being independent of operations and the different Risk Heads have direct access to the Board Chairperson/members without impediment.The complete Risk Management Report is set out on pages 84 to 113 of the Annual Report.

-

CORPORATE INTEGRITY AND WHISTLE BLOWING POLICY

The Bank has established a Corporate Integrity and Whistle Blowing Policy to promote an atmosphere of honesty and to encourage employees to conduct themselves in the best interests of the Bank.

A copy of the Corporate Integrity and Whistle Blowing Policy is available on the Bank’s website:

PRINCIPLE SIX – REPORTING WITH INTEGRITY

FINANCIAL

The Directors are responsible for preparing the financial statements in accordance with International Financial Reporting Standards, International Accounting Standards and Companies Act 2001. The Directors must ensure that the provisions of the Companies Act 2001, the Banking Act 2004 and Financial Reporting Act 2004 are complied with. They must also ensure that the financial statements are free from errors, material misstatements or irregularities and that any non-adherence is disclosed, explained and quantified.

SUSTAINABILITY

With the deployment of its sustainability strategy since 2016, AfrAsia Bank has been very active in the developments of its four pillars: Marketplace, Workplace, Social and Environmental Responsibilities.

Last year marked a milestone in the sustainability journey of the Bank with the publication of its first Integrated Report. The Integrated Reporting framework serve to guide AfrAsia in its strategy and provides clarity on how the six capitals are processed by the Bank to create value. The Integrated Report 2018 was classified at an advanced level in UNGC.

Financial Capital is the value of money that the Bank obtains from providers of capital that is used to support business activities. Profits are then generated for distribution amongst its stakeholders and for retention to fund business activities.

Manufactured Capital is the Bank’s tangible and intangible infrastructure, including IT assets, used for value creation through business activities.

Intellectual Capital refers to the collective knowledge, research, thought leadership, brand management and intellectual property used to support business activities and lead public discourse on global challenges.

Human Capital refers to the employees’ competencies, knowledge and experience and their capability to utilize these to meet stakeholder needs. The Bank puts its People at the forefront of its strategy and our Human Resources team is developing several strategies towards being the Employer of Choice in Mauritius.

Social and Relationship Capital refers to the relationships the Bank creates with its customers, investors, regulators, suppliers and community at large to create societal values as a responsible corporate citizen.

Natural Capital refers to the natural resources that the Bank uses to create value for its stakeholders, as well as climate finance it mobilizes to promote natural resource preservation and environmental mitigation.

Additionally, the Bank conducted its first materiality assessment to engage actively with its stakeholders on sustainability topics.

As from April 2019, AfrAsia is also a member of the Global GRI community.

Should you need a paper copy of AfrAsia Bank’s Sustainability Report 2019, please contact the Corporate Sustainability & CSR Team at This email address is being protected from spambots. You need JavaScript enabled to view it. or via phone (+230) 403-5500. You may also contact us via post [4th Floor NeXTeracom Tower III / Ebene 72201 / Mauritius]. You are requested to provide your full name and full postal address.

The Annual Report is published in full on the Bank’s website.

The financial statements are set out in Section B of the Annual Report.

The complete Risk Management Report is set out on pages 84 to 113 of the Annual Report.

PRINCIPLE SEVEN – AUDIT

DIRECTORS’ RESPONSIBILITIES

The Directors are responsible for the preparation and fair presentation of the financial statements in accordance with International Financial Reporting Standards and all the requirements of the Mauritius Companies Act 2001, the Banking Act 2004 and the Financial Reporting Act 2004 and for such internal controls as the Directors determine are necessary to enable the preparation of financial statements that are free from material misstatements, whether due to fraud or error. Any deviations on the above will be reported in the independent auditor’s report attached to the financial statements.

Statement of compliance

SECTION 75(3) OF THE FINANCIAL REPORTING ACT 2004)

AfrAsia Bank Limited and its Group Entities

Year ended 30 June 2019

We, the Directors of AfrAsia Bank Limitcd, confirm that to the best of our knowledge AfrAsia Bank Limited and its Group Entities have complied with all of its obligations and requirements under the National Code of Corporate Governance 2016 in all material aspects except for Principle 4. The reason for non-compliance is as per below.

Area of Non-Compliance

Principle 4 | Recommendation of the Code of Corporate Governance with respect to “Board Evaluation and Development” indicates that the Board is encouraged to undertake a formal, regular and rigorous evaluation of its own performance and that of its committees and individual Directors and produce a development plan on an annual basis. Reason for AfrAsia non-compliance: No Board appraisal exercise has been performed for the year under review due to recent changes in directors. The exercise will be launched once the new directors are more familiar with the Bank and its activities. |

Date: 19 September 2019